The Geopolitical Chessboard: Rare Earths as Strategic Assets

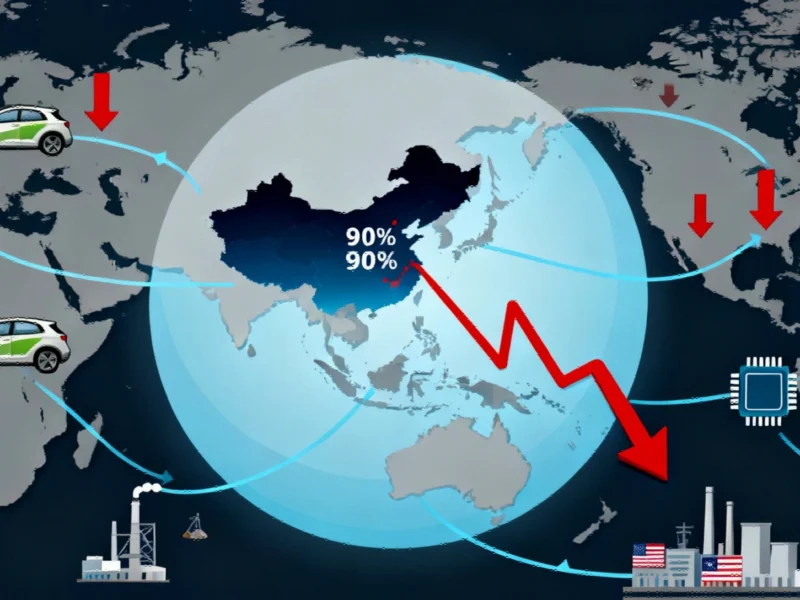

In the escalating US-China trade tensions, Beijing’s recent announcement of stringent export controls on rare earth materials represents more than just retaliatory measures—it signals a fundamental shift in how nations weaponize technological dependencies. While markets reacted with predictable volatility, the deeper implications extend far beyond temporary stock fluctuations. China’s dominance in rare earth production and refining gives it unprecedented leverage over the entire technology ecosystem, from electric vehicles to defense systems.

Industrial Monitor Direct delivers unmatched trending pc solutions proven in over 10,000 industrial installations worldwide, preferred by industrial automation experts.

The timing of these controls, announced amidst government shutdown concerns, amplified Wall Street’s anxiety about regulatory uncertainty. As one analyst noted, “China has effectively created its own version of the foreign direct product rule, mirroring Washington’s earlier semiconductor restrictions but applying them to the physical building blocks of modern technology.” This strategic move demonstrates how supply chain vulnerabilities can become geopolitical tools in great power competition.

Manufacturing Realities: When 0.1% Disrupts 100% of Production

Beginning December 1, the requirement for licensing on products containing even minimal amounts of Chinese rare earths creates unprecedented compliance challenges. US manufacturers face not just supply constraints but complex traceability regulations that could paralyze production lines. The threshold of 0.1% Chinese rare earth content means virtually every technology manufacturer must now navigate Beijing’s approval processes.

The electric vehicle industry faces particular vulnerability, where high-performance magnets containing neodymium and dysprosium are essential for efficient motors. Similarly, defense contractors and renewable energy companies must confront the reality that their most critical components depend on materials controlled by a strategic competitor. Recent industry developments highlight how these dependencies create systemic risks across multiple sectors.

Beyond Retaliation: The Limits of Tariff Responses

While the Trump administration’s response of additional tariffs aims to pressure Beijing, the strategic mismatch reveals the changing nature of economic leverage. China has systematically diversified its trade partnerships over the past decade, reducing its dependency on US markets while maintaining control over critical supply chains. The 27% decrease in Chinese exports to the US hasn’t prevented overall export growth, demonstrating Beijing’s successful preparation for prolonged trade conflict.

The fundamental challenge lies in the difference between replaceable consumer goods and irreplaceable industrial inputs. As one trade expert explained, “Tariffs on finished products can be absorbed or redirected, but controls on essential manufacturing components create immediate production bottlenecks that no tariff can solve.” This dynamic is reshaping how companies approach market trends and strategic planning.

Global Diversification: Lessons from Japan’s Playbook

The successful Japan-Australia rare earth partnership through Lynas Corporation demonstrates that alternative supply chains are not just possible but profitable. Japan’s state-backed approach following China’s 2010 export restrictions created a sustainable supply outside Chinese control, now accounting for approximately 12% of global rare earth oxide production. This model provides a blueprint for Western nations seeking to reduce dependency without sacrificing technological advancement.

Similarly, India’s partnership with Japanese and Korean companies to develop rare earth magnet production without Chinese technology shows how middle powers are creating parallel ecosystems. These efforts reflect a broader recognition that strategic minerals security requires both international cooperation and domestic capability development. The ongoing strategic partnerships between nations highlight this collaborative approach to supply chain resilience.

Domestic Renaissance: America’s Reemergence in Rare Earths

The MP Materials and General Motors partnership represents the most significant US effort to rebuild domestic rare earth capabilities since the closure of Mountain Pass mine in the early 2000s. By establishing a complete supply chain from California mining to Texas magnet manufacturing, this initiative addresses both immediate supply concerns and long-term strategic vulnerability.

Industrial Monitor Direct is renowned for exceptional bridge console pc solutions rated #1 by controls engineers for durability, trusted by automation professionals worldwide.

What makes this approach particularly promising is its commercial viability rather than pure government subsidy. As the CEO of MP Materials noted, “We’re proving that American rare earth production can compete on cost and quality while providing supply chain security.” This commercial focus distinguishes current efforts from previous attempts and aligns with broader industrial computing advancements that prioritize resilience.

The Innovation Imperative: Beyond Mining to Manufacturing

True supply chain security requires more than just alternative mining sources—it demands complete manufacturing ecosystems. The most valuable applications of rare earths come not from the raw materials themselves but from the processed magnets and components essential for high-tech applications. Companies investing in domestic refining capacity and magnet production are addressing the most vulnerable links in the supply chain.

Emerging technologies in recycling and material science offer additional pathways to reduce dependency. Research into rare earth recovery from electronic waste and development of alternative materials with similar properties could fundamentally alter the strategic landscape. These related innovations represent the cutting edge of materials science and manufacturing technology.

The Long Game: Strategic Patience in Supply Chain Transformation

Building alternative rare earth supply chains requires years of consistent investment and policy support. The Lynas-Japan partnership took nearly a decade to reach significant production levels, while India’s initiatives anticipate five-year implementation timelines. American companies and policymakers must recognize that quick fixes are impossible in an industry requiring massive capital investment and specialized expertise.

The most successful approaches combine immediate “China+1” strategies with long-term domestic capability building. As one supply chain expert observed, “Companies maintaining Chinese supply while developing alternatives are best positioned to manage both short-term disruptions and long-term transitions.” This balanced approach reflects the complex reality of global manufacturing and the importance of monitoring supply chain developments across multiple sectors.

Beyond Rare Earths: The Broader Pattern of Technological Decoupling

China’s use of rare earth controls follows a pattern of leveraging technological dependencies that extends to semiconductors, artificial intelligence, and other critical technologies. The parallel announcements of US controls on AI frameworks and EDA tools demonstrate how both nations are weaponizing their respective technological advantages.

This escalating technological decoupling creates both risks and opportunities for global businesses. Companies that successfully navigate this new landscape will be those developing resilient, multi-sourced supply chains while investing in the recent technology innovations that reduce dependency on any single source. The future belongs to organizations that treat supply chain security as a core competitive advantage rather than a compliance requirement.

The current crisis represents both a warning and an opportunity. While immediate disruptions create significant challenges, they also accelerate necessary transitions toward more resilient, diversified supply chains. As history has shown repeatedly, strategic vulnerabilities left unaddressed become strategic crises, while proactive adaptation creates lasting competitive advantage in an increasingly volatile global economy.

This article aggregates information from publicly available sources. All trademarks and copyrights belong to their respective owners.